Simplifying IR35: What you need to know

17 Dec, 202512 minutes

Reformed in 2017 and updated in 2021 across the public sector and private sector respectively, IR35 (AKA the off-payroll working rules) is a piece of legislation designed to clamp down on contractors paying less tax due to self-employment, but who are in fact “disguised employees”.

To this day there remains some confusion around the topic of IR35 compliance, but it’s no less important to understand how it affects your business – misunderstanding it (or ignoring it) could lead to harsh consequences.

We’ll be breaking down what IR35 is, who it affects and how to understand your or your contractors’ (if you engage them) IR35 status.

*Disclaimer – the following is a general guide to IR35 and status determinations. IR35 status and responsibilities will differ for each engagement. Please make sure you seek professional advice if you’re unsure.

What is IR35?

IR35 is a set of rules (legislation) that were introduced to essentially crack down on contractors who were treated like employees day-to-day (i.e. line managed or enjoyed benefits like holiday and sick pay or attending work events at no cost etc.) but who presented as self-employed for tax purposes – i.e. paying less tax and NICs.

The off-payroll working (OPW) rules are there to assess whether a contractor is genuine, rather than a “disguised employee”. The aim is to close a loophole that allowed contractors and freelancers to pay less tax by getting paid through an intermediary - like a personal service company (PSC) - while being treated like regular employees.

Who needs to know about IR35?

In general, anyone in the supply chain for the provision of services by a contractor could be affected, including:

- workers who provide their services through their own intermediary to a client (limited company/PSC, partnership or another individual)

- a client who receives services from a worker through an intermediary – this includes all public sector clients and medium-large private sector clients

- an agency or other supplier providing workers’ services through an intermediary

The 2017 IR35 reform and 2021 IR35 reform placed the responsibility of PAYE on the deemed employer (sometimes “the fee-payer” or “party immediately above the worker’s intermediary”) – it used to be on the contractor.

Though, if the client falls outside the requirements to be the deemed employer, the responsibility for correct PAYE remains with the contractor’s intermediary (whether that’s their own limited company or an agency).

What does IR35 status mean?

For any contractor engagement, it’s important to assess IR35 status and whether it falls inside or outside IR35 rules. This is based on things like working practices and contractual relationships and will determine whether the engagement falls within IR35 rules or outside the rules.

It’s important to remember that IR35 status applies per engagement not per contractor. A contractor could work on multiple contracts, but each one could have a different status based on how they work with the end client involved in the engagement.

What does ‘inside IR35’ mean?

‘Inside IR35’ means that an engagement falls within the requirements for the off-payroll working rules to apply. A contract engagement determined as ‘inside IR35’ means that factors like how a contractor provides a service and how they engage with the client is likened to that of a permanent worker (we’ll look more at factors below). The contractor will be classed as an employee for tax purposes and subsequently subject to PAYE accordingly. They will pay income tax and national insurance contributions at roughly the same rates as a regular employee.

What does ‘outside IR35’ mean?

‘Outside IR35’ means that an engagement falls outside the requirements and the off-payroll working rules don’t apply. An ‘outside IR35’ status means that an engagement has been deemed a genuine business relationship, and the contractor is genuinely self-employed for the purpose of tax in relation to the contract in question. This means they work independently while remaining responsible for paying their own taxes and national insurance contributions.

How is IR35 status determined?

We alluded to “factors” above – things that can combine to suggest a contractor engagement is either ‘inside’ or ‘outside’ IR35. It’s important to note that, unfortunately, it’s not completely black and white and there can be varying factors and circumstances to compare an engagement with. The main ones include:

- Right of substitution (or ‘personal service’): A contractor’s right to provide a replacement to perform the service they’re performing.

- Mutuality of obligation (MOO): In its purest form, MOO refers to an obligation for the client to give a contractor work and for them to do it.

It’s far from simplistic, but it essentially asks if a contractor is obliged to provide services on request or are they free to say no to work? And is a client expected to keep offering work, or are they free to end the working relationship once an assignment is complete?

- Control: This relates to the autonomy a contractor has over the services they deliver – the control they have over how they complete the work, where they work (e.g. home vs office) or what hours they work (e.g. on a rota vs managing their own time).

Minor status tests

On top of the ‘big deal’ factors like the ones above, other day-to-day things may also suggest if an engagement is ‘inside’ or ‘outside’ IR35. These are often referred to as minor IR35 status tests. Using examples for a contractor engagement ‘outside IR35’, some of the tests include:

- Genuine business: a contractor can demonstrate that they run a genuine business on its own account e.g. has its own website, branding, registered business premises, be VAT registered and have business insurance.

- Employee benefits: a contractor shouldn’t be seen to get any benefits typically associated with employment, like holiday pay, sick pay, memberships, company pension scheme, private health or even invites to Christmas parties!

- Company integration: a contractor should act as a separate entity to a client business (like an external visitor). This could be things like wearing a visitor lanyard, not having a dedicated desk and not being held to a client’s working hours.

- Contract termination: the contract of engagement should be terminatable at any point either immediately or with a short notice period. This can be by either the contractor/their intermediary or the end client.

- Financial risk: if running a genuine business, a contractor would face financial risk when entering an engagement. They could face losing income if the client fails to pay/cancels the work early or have to use their own time to fix mistakes at their own expense.

- Exclusivity: the contractor isn’t tied into exclusive working relationships with clients. They control their own time and can provide services for multiple clients at once.

This list isn’t exhaustive and there are a few more minor IR35 status tests to be aware of.

What does ‘inside’ or ‘outside’ IR35 look like?

To put this into context (and hopefully make it more digestible), here are examples of circumstances that could suggest ‘inside IR35’ and ‘outside IR35’.

Generally speaking, a contractor’s engagement is ‘inside IR35’ (a “disguised employee”) if most of the following applies:

- They have to do the work themselves and can’t suggest providing somebody else in their absence

- They have their working hours dictated by someone else

- Someone else can tell them what tasks to complete at any given time, how to complete them and the location they need to work in

- They’re eligible for overtime pay

- They’re eligible for a discretionary bonus (not included in the contract for project milestones)

On the other hand, an engagement may be considered ‘outside IR35’ if most of the following applies to the contractor:

- They can hire another person at their own expense to do the work for them

- They risk their own money

- They provide their own equipment like the main equipment needed to carry out work

- They control how, when and where they carry out work

- They carry out the work for a fixed fee regardless of time spent

- They work for several different clients

- They have to make fixes and amends to work (if unsatisfactory) at their own expense

What is the small business’ exemption for IR35?

Under the off-payroll rules, medium and large businesses must assess the IR35 status of contractors they engage. Small businesses, however, don’t have to. Instead, the contractor’s own limited company remains responsible for determining their IR35 status. This exemption exists to reduce the admin burden on smaller firms, which often don’t have the resources to handle complex tax compliance.

*Note – ‘small’ businesses still need to do their due diligence, be certain they’re exempt from off-payroll workings, and provide evidence of their size.

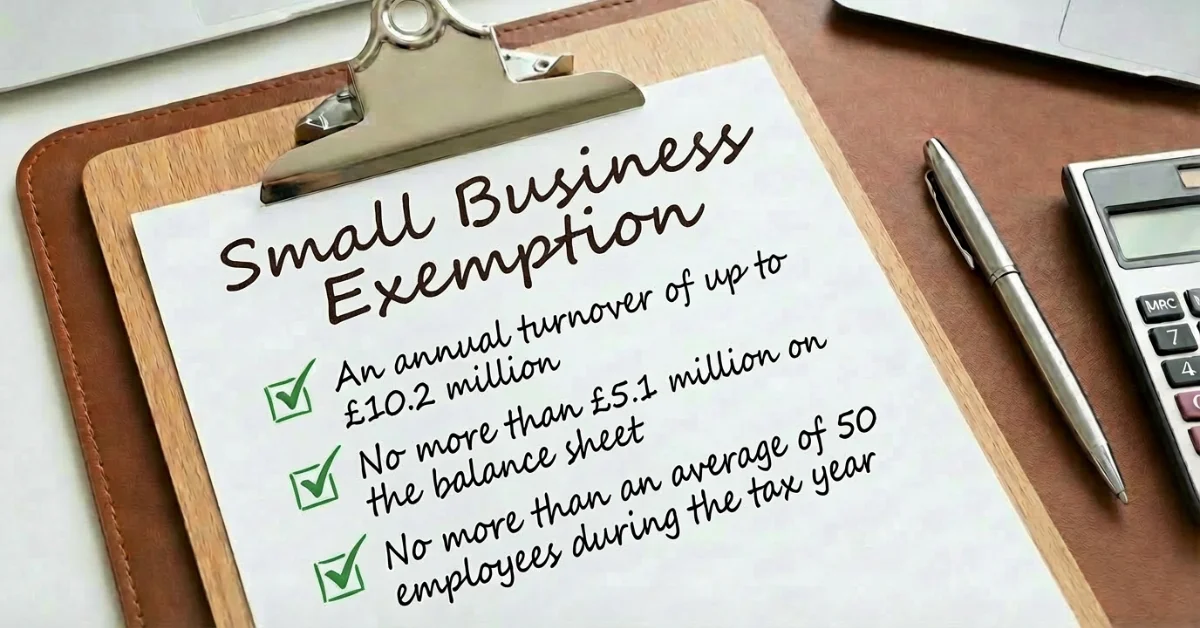

Who qualifies as a ‘small business’?

The definition of 'small business’ applies where a business meets two out of the three criteria:

- An annual turnover of up to £10.2 million

- No more than £5.1 million on the balance sheet

- No more than an average of 50 employees during the tax year

So, if you tick two of these boxes, you’re classed as “small” and the IR35 off-payroll rules don’t apply to you.

Changes to small business exemptions

It’s worth noting that these criteria are the rules at present. These thresholds changed from April 2025. These changes increased the thresholds to the following:

- Turnover of more than £15 million

- Balance sheet total of more than £7.5 million

- Monthly average of 50 employees (unchanged)

This means thousands of businesses will reclassify as ‘small’, though they likely won’t see the impact until 2027 – the exempt status will apply in the tax year after a full financial year.

For example, for an accounting period beginning on or after 6th April 2025 (and ending April 2026), the earliest filing date is January 2027.

It’s also worth noting that if your client’s organisation belongs to a group of companies and is, by definition, a small business, the parent organisation must also be small for the categorisation to stand.

Why is understanding IR35 important?

It’s crucial to understand how the off-payroll working rules (IR35) affect your own business and what you’re responsible for.

If an engaged contractor is caught working as a “disguised employee”, any and all points of the supply chain could be affected by any unpaid tax and NICs due plus interest on the amount. They could even get a penalty if HMRC can argue they haven’t undertaken any form of due diligence (e.g. taking reasonable care to understand obligations and take action accordingly).

Getting support with status determinations

The first thing to do is understand status determination statements (SDS) – a statement that declares both what a contractor engagement’s IR35 status is and the reasoning behind the conclusion.

You can use online tools to help generate them. HMRC developed their own Check Employment Status for Tax tool (CEST) to find out if a worker in an engagement should be deemed as employed or self-employed for tax purposes. Although, the CEST tool has faced some critiques recently.

The good news is that you can find reliable independent status tools that are designed with the user in mind and are often provided alongside expert support with your status determination.

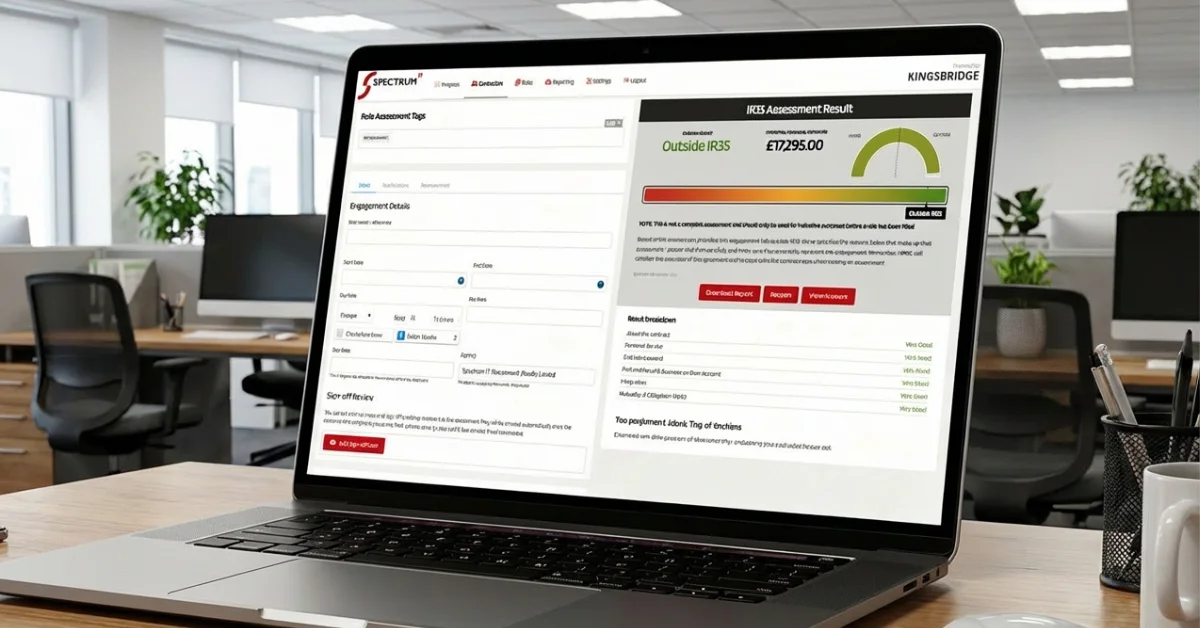

Navigating IR35 with Spectrum IT Recruitment & Kingsbridge

Navigating IR35 legislation and ensuring compliance can be challenging for contractors and businesses alike. Spectrum IT offers help and guidance with IR35, including status reviews with Kingsbridge’s award-winning IR35 Status Tool, which is one of the only solutions that’s supported by in-house consultants for borderline determinations.

If you’re looking for support navigating IR35 while securing the right talent for your project, our expert consultants can guide you through the compliance requirements and match you with the best candidates. Get in touch with Spectrum IT to get started.